All Categories

Featured

2 individuals acquisition joint annuities, which supply a guaranteed earnings stream for the remainder of their lives. If an annuitant dies during the circulation duration, the staying funds in the annuity might be handed down to a designated beneficiary. The certain alternatives and tax implications will depend upon the annuity contract terms and relevant regulations. When an annuitant dies, the interest earned on the annuity is taken care of differently relying on the sort of annuity. With a fixed-period or joint-survivor annuity, the passion continues to be paid out to the making it through recipients. A survivor benefit is an attribute that makes certain a payout to the annuitant's beneficiary if they pass away prior to the annuity repayments are worn down. Nonetheless, the availability and terms of the survivor benefit may vary relying on the specific annuity contract. A kind of annuity that stops all repayments upon the annuitant's fatality is a life-only annuity. Comprehending the terms of the survivor benefit prior to investing in a variable annuity. Annuities undergo taxes upon the annuitant's death. The tax treatment depends on whether the annuity is kept in a certified or non-qualified account. The funds undergo revenue tax in a qualified account, such as a 401(k )or individual retirement account. Inheritance of a nonqualified annuity typically results in taxation just on the gains, not the entire quantity.

If an annuity's marked beneficiary passes away, the outcome depends on the specific terms of the annuity contract. If no such recipients are assigned or if they, too

have passed away, the annuity's benefits typically revert generally the annuity owner's estate. If a recipient is not called for annuity advantages, the annuity proceeds usually go to the annuitant's estate. Annuity beneficiary.

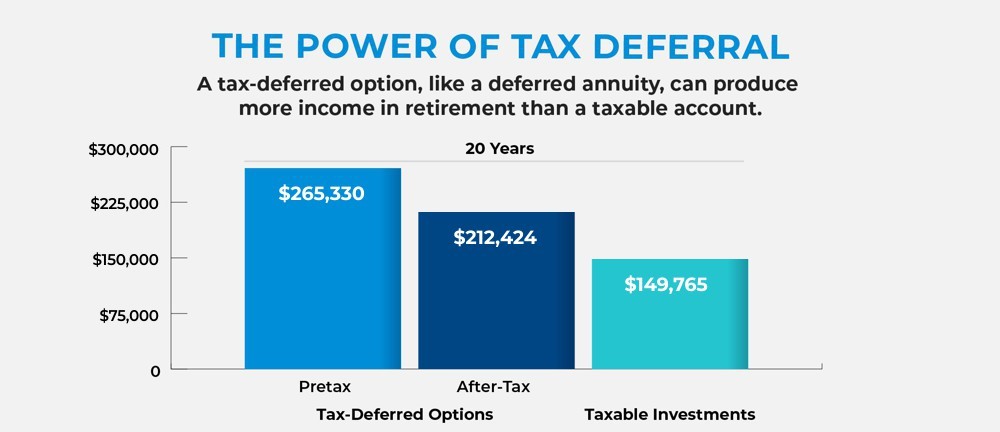

Annuity Income inheritance tax rules

This can supply greater control over just how the annuity advantages are distributed and can be part of an estate preparation method to manage and shield assets. Shawn Plummer, CRPC Retirement Planner and Insurance Policy Representative Shawn Plummer is a qualified Retirement Organizer (CRPC), insurance policy agent, and annuity broker with over 15 years of direct experience in annuities and insurance policy. Shawn is the owner of The Annuity Expert, an independent on the internet insurance coverage

company servicing customers across the United States. Through this system, he and his team aim to eliminate the guesswork in retirement preparation by helping people find the most effective insurance coverage at the most competitive prices. Scroll to Top. I recognize all of that. What I do not understand is just how previously getting in the 1099-R I was revealing a reimbursement. After entering it, I currently owe taxes. It's a$10,070 distinction in between the reimbursement I was expecting and the tax obligations I now owe. That seems extremely severe. At many, I would certainly have anticipated the reimbursement to decrease- not totally vanish. A financial advisor can help you decide exactly how ideal to take care of an inherited annuity. What takes place to an annuity after the annuity owner passes away depends upon the terms of the annuity contract. Some annuities merely stop dispersing earnings settlements when the owner dies. In many cases, however, the annuity has a fatality benefit. The beneficiary might obtain all the remaining money in the annuity or a guaranteed minimum payout, usually whichever is higher. If your moms and dad had an annuity, their agreement will certainly define that the recipient is and might

additionally have info concerning what payout alternatives are readily available for the survivor benefit. Practically all inherited annuities go through tax, however how an annuity is taxed depends upon its type, recipient condition, and repayment framework. Usually, you'll owe tax obligations on the difference between the initial costs made use of to purchase the annuity and the annuity's worth at the time the annuitant died. So, whatever portion of the annuity's principal was not currently taxed and any type of revenues the annuity collected are taxable as income for the recipient. Non-qualified annuities are acquired with after-tax dollars. Income repayments from a qualified annuity are dealt with as gross income in the year they're received and need to adhere to called for minimal distribution policies. If you acquire a non-qualified annuity, you will only owe taxes on the earnings of the annuity, not the principal used to purchase it. On the other hand, a round figure payout can have extreme tax obligation consequences. Because you're receiving the entire annuity at the same time, you have to pay taxes on the entire annuity because tax obligation year. Under specific conditions, you may be able to roll over an inherited annuity.

right into a retirement account. An inherited IRA is an unique retirement account made use of to disperse the possessions of a dead person to their recipients. The account is signed up in the departed individual's name, and as a beneficiary, you are not able to make additional payments or roll the inherited individual retirement account over to another account. Just qualified annuities can be rolledover into an inherited IRA.

{kind=link}

Latest Posts

Decoding How Investment Plans Work A Closer Look at Variable Vs Fixed Annuities What Is Fixed Interest Annuity Vs Variable Investment Annuity? Pros and Cons of Various Financial Options Why Variable A

Decoding How Investment Plans Work Everything You Need to Know About Deferred Annuity Vs Variable Annuity Defining the Right Financial Strategy Features of Smart Investment Choices Why Fixed Annuity V

Understanding Financial Strategies A Closer Look at Retirement Income Fixed Vs Variable Annuity Defining Fixed Interest Annuity Vs Variable Investment Annuity Benefits of Deferred Annuity Vs Variable

More

Latest Posts